What's new in Trade Master 9

The history of updates of the desktop, mobile and web platforms

Terminal

- New trading report improvements. Fixed display of the first value on the growth graph and drawdown calculations.

-

When opening accounts, traders receive several messages through the

internal email system. They provide credentials and useful information

about the platform capabilities and built-in services. We have updated

and enhanced these emails, translated them into 50 languages, and

completely updated the design.

- Optimized account deposit and withdrawal pages.

- Fixed volume change error when placing a new order. With some combinations of trading instrument settings, the field was not available for editing.

- Fixed display of broker agreement links in the demo account opening dialog.

- Updated user interface translations.

MQL5

- Fixed an error that could cause the MQL5 program to crash at startup under certain conditions.

Trade Master 9 Web Terminal

- Fixed display of Stop Loss and Take Profit values in trading history.

- Enhanced logging. New log messages display information on successful and failed connections.

- Fixed context menu operation in the Market Watch.

- Fixed display of notifications about operation results when trading from the Depth of Market.

- Fixed error which caused the indicator subwindow to be removed from the chart when calling the trading dialog.

- Fixed on-chart dragging of trading levels displayed on top of analytical objects.

Terminal

- Added display of monthly funds growth in new trading reports. To view the metrics, go to the Summary report and select the Balance mode.

- Fixed and improved display of the new trading report.

- ONNX Runtime updated to version 1.16. For release details, see GitHub.

- Updated user interface translations.

Trade Master 9 Web Terminal

- Fixed display of password change and account opening dialogs.

- Fixed display of Stop Loss and Take Profit values in history. An error could occur after the modification of the relevant levels.

- Added scroll in the risk warning dialog.

- Updated user interface translations.

- Other improvements and fixes.

Terminal

- New trading report improvements. Fixed the display of the total swaps value and the profit chart by symbols.

- Optimized deposit and withdrawal pages. For further details about the new platform integration with payment systems, please read the build 3950 release notes.

-

Optimized recalculations of financial operations across the entire

platform, including the strategy tester. Now profit, margins, and many

other parameters are calculated faster.

- Updated user interface translations.

MQL5

- Added Conjugate methods for complex, vector<complex> and matrix<complex> types. They implement complex conjugate operations.

//+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { complex a=1+1i; complex b=a.Conjugate(); Print(a, " ", b); /* (1,1) (1,-1) */ vectorc va= {0.1+0.1i, 0.2+0.2i, 0.3+0.3i}; vectorc vb=va.Conjugate(); Print(va, " ", vb); /* [(0.1,0.1),(0.2,0.2),(0.3,0.3)] [(0.1,-0.1),(0.2,-0.2),(0.3,-0.3)] */ matrixc ma(2, 3); ma.Row(va, 0); ma.Row(vb, 1); matrixc mb=ma.Conjugate(); Print(ma); Print(mb); /* [[(0.1,0.1),(0.2,0.2),(0.3,0.3)] [(0.1,-0.1),(0.2,-0.2),(0.3,-0.3)]] [[(0.1,-0.1),(0.2,-0.2),(0.3,-0.3)] [(0.1,0.1),(0.2,0.2),(0.3,0.3)]] */ ma=mb.Transpose().Conjugate(); Print(ma); /* [[(0.1,0.1),(0.1,-0.1)] [(0.2,0.2),(0.2,-0.2)] [(0.3,0.3),(0.3,-0.3)]] */ }

- Added handing of ONNX model outputs of the 'Sequence of maps' type.

For ONNX models that provide Map sequences in the output layer (ONNX_TYPE_SEQUENCE of ONNX_TYPE_MAP), a dynamic or fixed array of structures should be passed as the output parameter. The first two fields of this structure must match the ONNX_TYPE_MAP key and value types and be fixed or dynamic arrays.

Consider the iris.onnx model created by the following Python script:

from sys import argv data_path=argv[0] last_index=data_path.rfind("\\")+1 data_path=data_path[0:last_index] from sklearn.datasets import load_iris iris_dataset = load_iris() from sklearn.model_selection import train_test_split X_train, X_test, y_train, y_test = train_test_split(iris_dataset['data'], iris_dataset['target'], random_state=0) from sklearn.neighbors import KNeighborsClassifier knn = KNeighborsClassifier(n_neighbors=1) knn.fit(X_train, y_train) # Convert into ONNX format from skl2onnx import convert_sklearn from skl2onnx.common.data_types import FloatTensorType initial_type = [('float_input', FloatTensorType([None, 4]))] onx = convert_sklearn(knn, initial_types=initial_type) path = data_path+"iris.onnx" with open(path, "wb") as f: f.write(onx.SerializeToString())

Open the created onnx file in MetaEditor:

The Map sequence is passed as "output_probability". It has a key of INT64 type (which corresponds to long in MQL5) and the float type value. To receive data from this output, declare the following structure:

struct MyMap { long key[]; float value[]; };

Here we used dynamic arrays with appropriate types. In this case, we can use fixed arrays because the Map for this model always contains 3 key+value pairs.

Since the Map sequence is returned, an array of such structures should be passed as a parameter for receiving data from output_probability output. This array can be dynamic or fixed, in accordance with the properties of a particular model. Example:

//--- declare an array to receive data from the output layer output_probability MyMap output_probability[]; ... //--- model running OnnxRun(model,ONNX_DEBUG_LOGS,float_input,output_label,output_probability);

MetaEditor

- Fixed display of output types in the ONNX model viewer.

Trade Master 9 Web Terminal build 3980

- Added Contact Broker section in the web terminal's main menu.

- Added error handling for SSL authentications. This authentication type is not supported in the web terminal. One-time passwords can be used instead.

- Fixed desktop platform download link in the main menu.

- Fixed

accounts managing dialog. If the broker does not provide the demo or

real account opening option, the relevant menu item will be hidden.

Terminal

- Added support for balance operations for

depositing/withdrawing funds from a trading account directly in the

client terminal.

We have added integration of the most popular payment systems directly into the Trade Master 9 platform, which allows brokers to provide traders with a new level of service. When depositing or topping up, simply select the method that suits you best and complete the transaction. For more convenience, traders can save selected cards so as not to enter card details each time. Brokers do not store payment details and card numbers. The payment data entered by a user is sent over a secure channel to the user-selected payment system.

The new functionality provides traders with the opportunity to manage funds in one click without leaving the client terminal.

-

Completely revamped the trading history report. Now it is more easy to

view. We have revised the approach to presenting information and

converted dry statistical reports into interactive graphs and diagrams.

The work is still in progress, but you can evaluate the changes already.

To view trading statistics, click Reports in the View menu.

The report is divided into four tabs, each containing aggregated information:- Summary — trading summary: account data, overall profit and loss, deposits and withdrawals, balance, growth and dividends graphs and others.

- Profit/Lost — data on profitable and losing trades. The parameter is divided by types of trading (manual, algorithmic and copying trades). The results can be analyzed in terms of trades or money by months and years.

- Long/Short — dynamic ratio of purchases and sales at specified periods of time, as well as Buy and Sell profitability.

- Symbols — analysis of trades by financial instruments. Here you will see which symbols you earn or lose on, how often you trade them, graphs of trades and monetary volumes for them.

New reports allow you to visually evaluate trading results in a variety of aspects by simply clicking on the tabs. Histograms, graphs and diagrams are interactive and provide additional information when hovering the mouse cursor. Our designers have put much effort into making reports as simple and clear as possible. Just give them a try!

- Added the usage of AVX2 instructions

in case they are supported by CPU. This allows for more efficient use

of CPU capabilities the terminal is launched on. Now, when installing or

updating, the terminal determines the CPU architecture on its own and

installs the most optimal version. During the launch, the terminal sends

a message (AVX/AVX2) to the log displaying the set of instructions the

terminal is built for.

Terminal Trade Master 9 x64 build 3914 started for MetaQuotes Software Corp. Terminal Windows 10 build 19045, 20 x Intel Xeon E5-2630 v4 @ 2.20GHz, AVX, 41 / 63 Gb memory, 58 / 280 Gb disk, UAC, GMT+2

Advanced Vector Extensions (AVX) is an extension of the x86 instruction set for Intel and AMD microprocessors proposed back in 2008. Further development has led to the appearance of AVX2 and AVX-512 (2013).

- In addition to the two versions of

Trade Master 9 terminals on X64 and AVX, we have released the third

version of the desktop terminal compiled with direct support for AVX2

commands. At the same time, ONNX models now also work with support for

AVX2 commands.

- Added display of links to the

broker's necessary regulatory documents. You can now obtain all the

necessary legal information from your broker directly in the client

terminal in Help / Terms & Conditions.

- Fixed 2FA authorization in case of the additional use of the extended authorization using certificates.

- Fixed display of internal mail messages when working on MacOS.

- Fixed display of the Signals window when working in Wine.

- Released new MetaTrader 4 and 5 installers for Linux.

- Added commands for visiting Linux and Mac terminal version download pages

in Help. For traders' convenience, we have created a special section of

the website with terminal versions for all platforms, as well as for

trading in a browser.

- Fixed embedding images into internal mail.

- Released new Trade Master 9 terminal installers for Mac with support for M1/M2 processors. Due to the transition to Wine 8.0.1, we strongly recommend that you remove old versions and install new ones. When using Wine versions older than 8.0.0, a message about the need for an update is displayed in the terminal log.

- Added "VPS Hosting

Speed Up" in the network scan menu indicating the ping to your trading

server. This allows you to clearly see how your network delays decrease

when renting a built-in VPS.

- Strengthened the requirements for minimum password complexity, namely:

- password length — at least 8 characters

- the password must contain at least 1 character in upper and lower case, at least 1 digit and at least 1 special character.

- Usable links in terminal logs. Now when double-clicking on lines with https links, users are sent to their browsers and the link is opened.

-

Fixed search for trading instruments in Market Watch. Now the symbol is

first searched by name, and then by other fields: description, ISIN,

etc.

- Fixed accounting for profit on trades when

calculating the balance in account trading history reports. In some

cases, the instrument type was not taken into account in the

calculations.

VPS Hosting

- Added the ability to send and run EX5 programs compiled under the x64/AVX/AVX2 command set. Programs for AVX512 are not supported on the built-in VPS.

- Increased the number of locations for renting the built-in VPS up to 27. Now the selection of the closest server has become even wider.

MQL5

-

Added control of compilation settings, including selection of extended

processor instruction sets — AVX, AVX2, AVX512 and FMA3.

Modern CPUs have a set of advanced instructions that significantly speed up mathematical calculations, but the vast majority of modern programs do not use these capabilities. We have added support for these instructions to the MQL5 language compiler, which allows for more efficient and faster code generation.

We have also added the ability to choose which type of instructions to compile an MQL5 program with. You can specify both general settings for single programs in MetaEditor Options, and apply personal ones in project settings:

- Added the ENUM_AVERAGE_MODE and ENUM_CLASSIFICATION_METRIC enumerations to the Matrix and Vector Methods.

- Added Set method for vectors.

- Revised OpenCL initialization - now it is initialized by the first actual use, not by loading an MQL5 program containing OpenCL functions.

- Fixed an error when calling the SocketIsConnected function.

- Fixed delay in calling the OnDeinit method when unloading custom indicators.

- Fixed a compiler error, which caused incorrect calculation of the string length in the indicator_label property leading to incorrect display of tooltips for graphical objects.

- Fixed the use of multi-line comments in the macro body. An example of a macro where the error occurred:

#define MACRO1 /* #define MACRO2 */ void OnStart() { #ifdef MACRO2 Print( 2 ); #else Print( 1 ); #endif }

- Fixed the order of parameters of the MathAtan2 function. The order now matches the similar function in C++.

- Added the new TERMINAL_CPU_ARCHITECTURE value to the ENUM_TERMINAL_INFO_STRING

enumeration. Also, added the __CPU_ARCHITECTURE__ macro — obtaining

the CPU architecture of the computer the terminal is running on. Example

of use:

void OnStart() { Print("CPU name: ",TerminalInfoString(TERMINAL_CPU_NAME)); Print("CPU cores: ",TerminalInfoInteger(TERMINAL_CPU_CORES)); Print("CPU architecture: ",TerminalInfoString(TERMINAL_CPU_ARCHITECTURE)); Print(""); Print("EX5 architecture: ",__CPU_ARCHITECTURE__); } CPU name: 12th Gen Intel Core i9-12900K CPU cores: 24 CPU architecture: AVX2 + FMA3 EX5 architecture: AVX

- Changed the extern modifier behavior. Now declaration of a variable with the extern modifier is a variable pre-declaration.

New restrictions: - The variable pre-declaration should not contain initialization. For

example, when compiling the code below, we get the error "X - extern

variable initialization is not allowed":

extern int X=0; void OnStart() { }

- The 'extern' variable should be declared in the

program without the 'extern' keyword. For example, when compiling the

code below, we get the error "unresolved extern variable X":

extern int X; void OnStart() { }

- When using 'extern', it is important to pay

attention to the initialization order, because a variable can be

accessed before it is initialized. For example, the following code will

yield "Y=0 X=5" in the log since initialization of variable Y occurs

before initialization of variable X:

extern int X; int Y=X; void OnStart(void) { Print("Y=",Y," X=",X); } int X=_Digits;

MetaEditor

- Added the usage of AVX2 instructions in case they are supported by CPU.

- Fixed an error occasionally causing freezes during compilation.

- Improved display of local variables when debugging.

Tester

- Added the usage of AVX2 instructions in case they are supported by CPU.

Updated user interface translations.

Fixed errors reported in crash logs.

Trade Master 9 Web Terminal build 3950

- Added display of the Ask price to the chart settings.

- Accelerated initial terminal loading.

- Added the ability to change the password.

- Added the ability to delete and save the password.

- Added a custom period for displaying trading history.

- Fixed forced password change.

- Fixed calculation of diff — the distance between the open price and TP/SL levels.

- Fixed ticks stop error when closing all orders/deals.

- Fixed display of Economic calendar events. Sometimes, they were not displayed on the chart despite the option being enabled.

- Fixed indicator reset when changing a chart symbol.

- Fixed an error in the form of opening a real account when confirming the phone/email.

- Added new translations and corrected existing ones.

Terminal

- Added support for the new order filling policy — Passive / Book or Cancel (BOC).

The BOC policy indicates that an order can only be placed in the Depth of Market (order book). If the order can be filled immediately when placed, this order is canceled. This policy guarantees that the price of the placed order will be worse than the current market price. BOC is used to implement passive trading: it is guaranteed that the order cannot be executed immediately when placed and thus it does not affect current liquidity. This filling policy is only supported for limit and stop limit orders in the Exchange Execution mode.

The availability of the new filling policy depends on the broker.

- The platform switches to using Microsoft Edge WebView2 for displaying the HTML content.

Compared to the outdated MSHTML, the new component significantly expands content displaying capabilities by providing access to modern technologies. The use of WebView2 improves the appearance of some platform sections, increases performance, and creates a more responsive interface. In particular, the new component will affect the Market, Signals and VPS sections.Full support for WebView2 was introduced in Windows 10. We strongly recommend that all users upgrade to the latest operating system version and install all available updates. The platform will continue to use MSHTML under Windows 7 and Wine, but the new features will not be available. The minimum recommended operating system version is Windows 10 21H2 (build 19044, November 2021).

- Improved Market

security system. Now, in order to run the product, the user must be

authorized in the platform with the same MQL5 account via which the

product was purchased. The account must be specified under the Tools \

Options \ Community section:

If no account or an invalid account is specified, the product will not start, and the following message will be printed in the platform journal:

'ProductName' requires active MQL5 account in Tools->Options->Community - Added Overview command to the history section context menu. The command opens a trading report for the account:

- Fixed display errors in the two-factor authentication dialog. If the terminal had several accounts with the same number but opened with different brokers, the account connection form could fail to display the one-time password field.

- Implemented faster rendering of indicators with the DRAW_COLOR_CANDLES display style.

- Fixed trading report creation errors. On-chart profit and equity values could be displayed incorrectly under certain conditions.

- Added display of Costs in the trading report. The value shows the total costs incurred when performing deals relative to the symbol's current mid-point price (mid-point spread cost). This is the amount which the trader lost due to the spread. The availability of this value depends on the broker.

- Updated UI translations.

- Improved stability under Wine, especially on macOS

systems. We recommend completely removing old terminals and

re-installing them:

- Accelerated package installation and updates downloading procedures. Improved analysis of AVX availability on the user's computer when selecting a distribution package.

- Enabled support for TLS 1.3 in web protocols. TLS 1.0 is considered deprecated and insecure and has therefore been disabled.

- Fixed accounting for agent commissions in trading history reports. The relevant transactions could be ignored when calculating the final profit.

- Fixed the inability to change the server in the account connection dialog. The issue arose when there were several accounts in the terminal with the same number from different brokers.

MQL5

- Added new STAT_COMPLEX_CRITERION value in the ENUM_STATISTICS enumeration. Use the property to obtain the calculated complex criterion value, as a result of optimization.

- Improved RegressionMetric

method used for calculating the regression metric based on the passed

matrix or vector. Added vector_true and matrix_true parameters for

passing true values which evaluate the predicted data quality.

double vector::RegressionMetric( const vector& vector_true, // true values const ENUM_REGRESSION_METRIC metric // metric ); double matrix::RegressionMetric( const matrix& matrix_true, // true values const ENUM_REGRESSION_METRIC metric // metric ); vector matrix::RegressionMetric( const matrix& matrix_true, // true values const ENUM_REGRESSION_METRIC metric, // metric const int axis // axis );

- Added the LinearRegression method. It returns a vector/matrix with calculated linear regression values for the passed vector/matrix.

vector vector::LinearRegression(); matrix matrix::LinearRegression( ENUM_MATRIX_AXIS axis=AXIS_NONE // axis along which regression is calculated );

Example:

vector vector_a; //--- fill the vector with prices vector_a.CopyRates(_Symbol,_Period,COPY_RATES_CLOSE,1,100); //--- get a linear regression vector vector_r=vector_a.LinearRegression();

The results are visualized in the graph:

- Added the HasNan method, which returns the number of NaN values in a matrix/vector.

ulong vector::HasNan(); ulong matrix::HasNan();

When comparing the appropriate pair of elements having NaN values, the Compare and CompareByDigits methods consider these elements equal, while in case of a usual comparison of floating-point numbers NaN != NaN.

-

Modified the OnnxTypeInfo structure which is used for operations with ONNX (Open Neural Network Exchange) models:

struct OnnxTypeInfo { ENUM_ONNX_TYPE type; // parameter type OnnxTensorTypeInfo tensor; // tensor description OnnxMapTypeInfo map; // map description OnnxSequenceTypeInfo sequence; // sequence description };

The data type is specified in the structure using new substructures:

- OnnxTensorTypeInfo — tensor

- OnnxMapTypeInfo — map

- OnnxSequenceTypeInfo — sequence

struct OnnxTensorTypeInfo { ENUM_ONNX_DATATYPE data_type; // data type in the tensor long dimensions[]; // number of elements }; struct OnnxMapTypeInfo { ENUM_ONNX_DATA_TYPE key_type; // key type OnnxTypeInfo type_info; // value type }; struct OnnxSequenceTypeInfo { OnnxTypeInfo type_info; // data type in the sequence };

Depending on OnnxTypeInfo::type (ONNX_TYPE_TENSOR, ONNX_TYPE_MAP or ONNX_TYPE_SEQUENCE), the relevant substructure is filled.

- Improved support for ONNX models.

- Added CopyIndicatorBuffer methods which enable the obtaining of indicator buffer data into a vector.

bool vector<T>::CopyIndicatorBuffer(long indicator_handle,ulong buffer_index,ulong start_pos,ulong count); bool vector<T>::CopyIndicatorBuffer(long indicator_handle,ulong buffer_index,datetime start_time,ulong count); bool vector<T>::CopyIndicatorBuffer(long indicator_handle,ulong buffer_index,datetime start_time,datetime stop_time);

- Fixed operations with arrays having two or more dimensions in the FrameAdd and FrameNext methods.

- Fixed CRedBlackTree::Remove Standard Library method.

- Implemented fixes in the Fuzzy Logic library.

MetaEditor

- Added integration with the advanced automatic coding assistant Copilot. Its operation is based on OpenAI models.

Enter a comment or part of a function and send a prompt. The neural

network will analyze the prompt and will offer coding options to

implement the idea.

Depending on the file type, the string "MQL5 language", "Python language" or "C++ language" is automatically inserted at each prompt beginning. Thus, the neural network will provide the result in the required language.

Copilot is currently free and is already enabled in the editor. There are several options available under Tools \ Options \ Copilot:

Payment settings:

- Use your MQL5 account: this option is currently available for free. Later, you will be able to pay for the subscription directly from your MQL5 account balance.

- Use an OpenAI key, if you have purchased a subscription and have the relevant key.

Prompt settings:

- Model — a neural network which will process your requests. text-davinci-003 and gpt-3.5-turbo are currently available. Support for gpt-4 will be added soon.

- Maximum tokens — the number of text units which the model can return in response to a prompt.

- Variability — affects how strictly the neural network will

follow the prompt. The bigger the value, the greater the result

randomness. This option corresponds to the temperature parameter in OpenAI models.

- Added ability to view the properties of ONNX models.

You can view the contents of the *.onnx file directly in the editor. As an example, find the project ONNX.Price.Prediction under Toolbox \ Public Projects and select Join in the context menu. The project will be downloaded to your computer and will appear in the Navigator.

- Added ability to visualize machine learning models and neural networks using Netron. This viewer supports popular models, including ONNX, TensorFlow Lite, Caffe, Keras and ncnn, among others.

To view a model, select its file in the Navigator and click "Open in Netron". If this utility is not installed, its GitHub page will open, from which you can download the relevant installer, according to your operating system. For example, use Netron-Setup-X.X.X.exe for Windows. If the program is installed, the model will immediately open for viewing from the Navigator.

Supported formats:

- armnn, caffemodel, circle, ckpt, cmf, dlc, dnn, h5, har, hd5, hdf5, hn, keras, kmodel,

- lite, mar, meta, mge, mlmodel, mlnet, mlpackage, mnn, model, nb, ngf, nn, nnp,

- om, onnx, ort, paddle, param, pb, pbtxt, pdiparams, pdmodel, pdopt, pdparams, prototxt, pt, pth, ptl,

- rknn, t7, tfl, tflite, tmfile, tm, tnnproto, torchscript, uff, xmodel

- Updated UI translations.

Tester

- Fixed calculation of the "Average losing trade" metric in the testing report. Previously, the calculation could erroneously include entry deals if commissions were charged for such deals.

- Improved custom commission options in the strategy tester. To set a symbol, specify its name rather than the entire path.

- Updated icons in the strategy tester. New metaphors will make them easier to understand.

Fixed errors reported in crash logs.

Web Terminal

- Improved trading history section:

- Added display of balance operations in the trading history, such as deposits and withdrawals, commissions, and adjustments.

- Added display of totals in the trading history: balance, profit, commission, deposits, withdrawals and number of orders, among others.

- Added ability to sort operations and filter the history by depth in the mobile version.

- Enhanced symbol contract specifications. The following information has been added: volume limit, tick size and value, initial and hedged margin.

- Improved color schemes:

- Pending orders are displayed in gray on the chart. The

position color depends on the direction: red for Sell and blue for Buy.

The new colors provide easier navigation especially if a lot of

operations are displayed on the chart.

- When viewing/editing a position, only this position and its

levels are highlighted, while all other positions and orders become

gray, and their levels are hidden from the price scale. Thus, it will be

easier to manage separate operations.

- The Stop Loss color has been changed from red to orange to avoid confusion with Sell positions.

- Improved on-chart icons indicating position closing time. A

green icon is used for positions closed by Take Profit and a red one is

used for those closed by Stop Loss.

- Added interface translations into Arabic, Bulgarian, Vietnamese,

Greek, Indonesian, Malay, Dutch, Persian, Polish, Thai, Ukrainian and

Hindi. The web terminal is now available in 24 languages.

- Fixed Turkish UI translations.

- Fixed modification and deletion of pending orders in the Web Terminal mobile version.

- Fixed on-chart 'closed market' tooltip.

- Fixed display of profits in the position close button in the trading dialog. The error occurred during partial closing.

- Fixed display of on-chart trading notifications.

- Fixed volume modification using arrows in the Depth of Market.

- Fixed error which could cause the settings of running indicators to be reset under certain conditions.

- Fixed username checks when opening new accounts. Previously, an apostrophe in the name was considered an error.

- Fixed processing of requotes. The dialog with the requoted prices might not be displayed under certain conditions.

- Fixed display of the Ichimoku Kinko Hyo indicator. The

Chikou-Span, Up Kumo and Down Kumo lines will be displayed with the

correct offset.

- Fixed initial margin checks when opening new orders. The error occurred in the hedging position accounting system.

- Fixed scrolling in the contract specification window.

MQL5.community

- The MQL5 Cloud Network website has been completely redesigned: https://cloud.mql5.com.

Learn how to use the processing power of thousands of computers around the world to optimize your trading strategies. With the MQL5 Cloud Network, even the heaviest computations can be completed in a matter of minutes. Visit the website and find out how to participate in the network and how to earn money by providing your computer resources.

- Improved screenshot section in Market

products. Authors can upload images up to 1920*1800 pixels to

demonstrate how applications work. The screenshot gallery has also been

updated. The carousel shows image thumbnails, and a click on them opens

full-sized images.

- Freelance section improvements. Users will now receive more tips when placing their first orders:

- Requirements specification examples and a reminder to add one

- Order creation instructions

- Template usage tips

These tips can assist you in creating the order and in receiving the desired result.

Terminal

- Fixed occasional incorrect platform log creation.

- Updated translations of the user interface.

MQL5

- Fixed checking global variables. When declaring identical variables in

different namespaces, the compiler gave an erroneous warning that the

variable was already declared.

Web Terminal

- Added user interface translation into Portuguese. The web terminal is now available in 12 languages.

- Fixed the dialog for adding Standard Deviation indicator.

- Minor fixes and improvements.

Web Terminal

- Added

UI translations into 10 widely spoken languages: Simplified and

Traditional Chinese, French, German, Italian, Japanese, Korean, Spanish,

Turkish and Russian. This list will be further expanded in future

versions. To switch the language, use the relevant menu:

- Optimized connection mechanism to the trade server.

MQL5

MQL5: Added COPY_TICKS_VERTICAL and COPY_RATES_VERTICAL flags for the CopyTicks, CopyTicksRange and CopyRates methods respectively.

By default, ticks and series are copied to the matrix along the horizontal axis, which means the data is added to the right, at the line end. In trained ONNX model running tasks, such a matrix needs to be transposed in order to feed the input data:

const long ExtOutputShape[] = {1,1}; // model's output shape const long ExtInputShape [] = {1,10,4}; // model's input shape #resource "Python/model.onnx" as uchar ExtModel[]// model as a resource //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ int OnStart(void) { matrix rates; //--- get 10 bars if(!rates.CopyRates("EURUSD",PERIOD_H1,COPY_RATES_OHLC,2,10)) return(-1); //--- input a set of OHLC vectors matrix x_norm=rates.Transpose(); vector m=x_norm.Mean(0); vector s=x_norm.Std(0); matrix mm(10,4); matrix ms(10,4);

By specifying the additional flag COPY_RATES_VERTICAL (COPY_TICKS_VERTICAL for ticks) when calling the method, you can eliminate the extra data transposition operation:

//+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ int OnStart(void) { matrix rates; //--- get 10 bars if(!rates.CopyRates("EURUSD",PERIOD_H1,COPY_RATES_OHLC|COPY_RATES_VERTICAL,2,10)) return(-1); //--- input a set of OHLC vectors

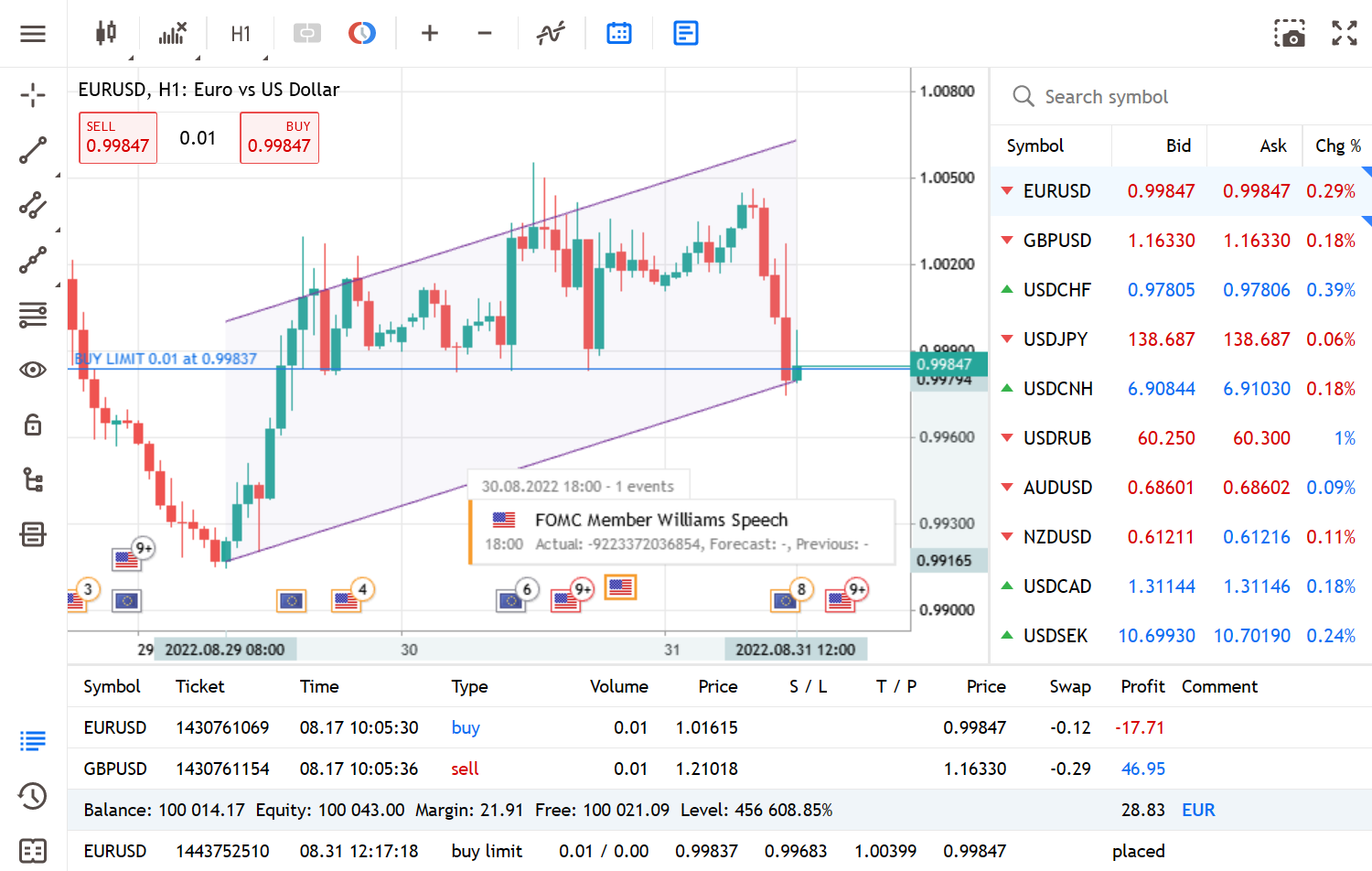

- New value in the ENUM_CHART_PROPERTY_INTEGER enumeration — CHART_SHOW_TRADE_HISTORY. The property controls the display of trades from the trading history on the chart. Use the ChartGetInteger and ChartSetInteger functions to obtain and set the property. For further details about the trades display on the chart, please read the platform documentation.

MetaEditor

- Fixed interface freezing which could occur during file compilation under certain conditions.

Terminal

- Fixed errors reported in crash logs.

Terminal

- Fixed total profit calculations in trading reports.

- Updated fundamental data for trading instruments available through the Market Watch window.

- Fixed trading platform launch under Wine 7.0.1 in Linux-systems.

- Fixed adding of symbols to the Market Depth via the search bar. A

symbol found by description could not be added to the list by clicking

on its line.

MQL5

- Added support for operations with ONNX models (Open Neural Network Exchange).

ONNX is an open-source format for machine learning models. This format is supported by many platforms, including Chainer, Caffee2 and PyTorch. Create an ONNX model using specialized tools, integrate it into your MQL5 application and use it to make trading decisions.

Descriptions of all supported functions are available in the documentation. An example of a test ONNX model is available in public projects in MetaEditor. Find the ONNX.Price.Prediction project in "Toolbox \ Public projects" and select Join in the context menu. The project will download to your computer and will appear in the Navigator:

Compile the project and run it on EURUSD H1 to see the result.

In addition to the model and the MQL5 code which runs it, the project also includes the PricePredictionTraining.py Python script. It shows how you can create an ONNX model yourself. To run the script, install Python on your computer and the required modules from the prompt line:

python.exe -m pip install --upgrade pipInstructions on how to use ONNX are available in the documentation.

python -m pip install --upgrade tensorflow

python -m pip install --upgrade pandas

python -m pip install --upgrade scikit-learn

python -m pip install --upgrade matplotlib

python -m pip install --upgrade tqdm

python -m pip install --upgrade metatrader5

python -m pip install --upgrade onnx==1.12

python -m pip install --upgrade tf2onnx

- Added support for General Matrix Multiplication

(GeMM). This algorithm speeds up calculations on some processor types

through parallelized tasks and optimized utilization of L1/L2/L3 caches.

The calculation speed is comparable with popular packages such as Math Kernel Library (MKL) and OpenBLAS. Detailed comparative tests will be published soon.

The new algorithm is currently supported in the matrix::GeMM method. If your processor supports AVX and FMA instructions (most processors released after 2013 support these instructions), the algorithm will be enabled automatically.

- Added ability to transfer matrices and vectors to DLL. This enables the import of functions which utilize the relevant types, from external variables.

Matrices and vectors are passed to a DLL as a pointer to a buffer. For example, to pass a matrix of type float, the corresponding parameter of the function exported from the DLL must take a float-type buffer pointer. For example:

MQL5

#import "mmlib.dll" bool sgemm(uint flags,matrix<float> &C,const matrix<float> &A,const matrix<float> &B,ulong M,ulong N,ulong K,float alpha,float beta); #import

C++

extern "C" __declspec(dllexport) bool sgemm(UINT flags,float *C,const float *A,const float *B,UINT64 M,UINT64 N,UINT64 K,float alpha,float beta)

In addition to buffers, you should pass matrix and vector sizes for correct processing.

-

Added new CopySeries function for copying synchronized timeseries from MqlRates into separate arrays.

The CopySeries function allows obtaining only the necessary timeseries into different specified arrays during one call, while all of timeseries data will be synchronized. This means that all values in the resulting arrays at a certain index N will belong to the same bar on the specified Symbol/Timeframe pair. Therefore, there is no need for the programmer to additionally synchronize the received timeseries by the bar opening time.

Unlike CopyRates, which returns the full set of timeseries as an MqlRates array, the CopySeries function allows obtaining specific required timeseries into separate arrays. This can be done by specifying a combination of flags to select the type of timeseries. The order of the arrays passed to the function must match the order of the fields in the MqlRates structure:

struct MqlRates { datetime time; // period beginning time double open; // open price double high; // high price for the period double low; // low price for the period double close; // close price long tick_volume; // tick volume int spread; // spread long real_volume; // exchange volume }

Thus, if you need to get the values of the 'time', 'close' and 'real_volume' timeseries for the last 100 bars of the current Symbol/Timeframe, you should use the following call:

datetime time[]; double close[]; long volume[]; CopySeries(NULL,0,0,100,COPY_RATES_TIME|COPY_RATES_CLOSE|COPY_RATES_VOLUME_REAL,time,close,volume);

The order of the arrays "time, close, volume" must match the order of the fields in the MqlRates structure. The order of values in the rates_mask is ignored. The mask could be as follows:

COPY_RATES_VOLUME_REAL|COPY_RATES_TIME|COPY_RATES_CLOSE

Example

//--- input parameters input datetime InpDateFrom=D'2022.01.01 00:00:00'; input datetime InpDateTo =D'2023.01.01 00:00:00'; input uint InpCount =20; //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart(void) { //--- arrays to get timeseries from the Rates structure double open[]; double close[]; float closef[]; datetime time1[], time2[]; //---request close prices to a double array ResetLastError(); int res1=CopySeries(NULL, PERIOD_CURRENT, 0, InpCount, COPY_RATES_TIME|COPY_RATES_CLOSE, time1, close); PrintFormat("1. CopySeries returns %d values. Error code=%d", res1, GetLastError()); ArrayPrint(close); //--- now also request open prices; use float array for close prices ResetLastError(); int res2=CopySeries(NULL, PERIOD_CURRENT, 0, InpCount, COPY_RATES_TIME|COPY_RATES_CLOSE|COPY_RATES_OPEN, time2, open, closef); PrintFormat("2. CopySeries returns %d values. Error code=%d", res2, GetLastError()); ArrayPrint(closef); //--- compare the received data if((res1==res2) && (time1[0]==time2[0])) { Print(" | Time | Open | Close double | Close float |"); for(int i=0; i<10; i++) { PrintFormat("%d | %s | %.5f | %.5f | %.5f |", i, TimeToString(time1[i]), open[i], close[i], closef[i]); } } /* Result 1. CopySeries returns 0 values. Error code=0 [ 0] 1.06722 1.06733 1.06653 1.06520 1.06573 1.06649 1.06694 1.06675 1.06684 1.06604 [10] 1.06514 1.06557 1.06456 1.06481 1.06414 1.06394 1.06364 1.06386 1.06239 1.06247 2. CopySeries returns 0 values. Error code=0 [ 0] 1.06722 1.06733 1.06653 1.06520 1.06573 1.06649 1.06694 1.06675 1.06684 1.06604 [10] 1.06514 1.06557 1.06456 1.06481 1.06414 1.06394 1.06364 1.06386 1.06239 1.06247 | Time | Open | Close double | Close float | 0 | 2023.03.01 17:00 | 1.06660 | 1.06722 | 1.06722 | 1 | 2023.03.01 18:00 | 1.06722 | 1.06733 | 1.06733 | 2 | 2023.03.01 19:00 | 1.06734 | 1.06653 | 1.06653 | 3 | 2023.03.01 20:00 | 1.06654 | 1.06520 | 1.06520 | 4 | 2023.03.01 21:00 | 1.06520 | 1.06573 | 1.06573 | 5 | 2023.03.01 22:00 | 1.06572 | 1.06649 | 1.06649 | 6 | 2023.03.01 23:00 | 1.06649 | 1.06694 | 1.06694 | 7 | 2023.03.02 00:00 | 1.06683 | 1.06675 | 1.06675 | 8 | 2023.03.02 01:00 | 1.06675 | 1.06684 | 1.06684 | 9 | 2023.03.02 02:00 | 1.06687 | 1.06604 | 1.06604 | */ }

- Fixed OrderSend function operation. The function request could return an incorrect order ticket if the same account was used simultaneously on several platforms.

- Fixed import of EX5 libraries. An error

occurred if the name of the imported library matched the name of the

file into which it was imported.

MetaEditor

- Added sending of push notifications to shared project members. The new option can notifies users of changes in project settings and files. To enable notifications, enter your MetaQuotes ID under the "Settings \ Security" section of your MQL5.community profile.

- Updated file icons in the Navigator. New, simpler metaphors will make them easier to understand.

Tester

- Fixed an error which caused the input string parameter to be truncated if it contained the "|" character.

Trade Master 9 Web Terminal build 3620

-

Added

ready-made color templates for the web terminal interface. The

templates affect the display of chart bars and lines, and the prices in

the Market Watch and account financial statements. Our design team has

prepared color template presets, based on your suggestions and on

traditional color combinations.

-

Redesigned symbol specification window. Trading instrument data has been rearranged into logical blocks for ease of viewing.

- Fixed opening of real accounts via the web terminal. The server could return an error after filling out a registration form.

- Fixed an error in the trading dialog. If the user closed a position by pressing the X button in the Toolbox window while the position modification dialog was open, the dialog contents were not reset. After the update, the dialog will automatically reset to a new order placing mode in this case.

- Fixed display of the Server field in the account management dialog.

- Fixed display of the current timeframe on the toolbar.

- Fixed display of volumes in terms of underlying asset units, in the trading dialog.

- Fixed modification of Stop Loss and Take Profit levels. Modifying one of the values could reset the second one under certain conditions.

- Fixed display of investment risk warnings.

- Added ability to place stop and stop-limit orders from the chart.

Only limit orders were available in earlier versions. Select the required type by successively pressing the button in the bottom chart panel.

- Added

ability to access position closing or pending order deletion features

from the chart. Select a position or an order level on the chart, and

the relevant command will appear in the lower trading panel:

- Improved

functionality which shifts the right border of the price chart. To

change the shift, simply scroll the chart to the last price until a

vertical separator appears. Next, drag the triangle at the bottom chart

scale:

- Added

ability to copy analytical objects on the chart. This enables faster

chart markup. Open the object menu with a long press and select "Copy":

- Added

ability to manage the display of indicators on different timeframes. If

the indicator is not suitable for certain chart periods, it can be

hidden to free up space on the screen for other analytical tools.

- Added display of symbol commissions in the instrument specification window.

- Added

password recovery link. An account password can only be restored via

the relevant broker. The link shows the broker's contact details.

- Added ability to share a link to an MQL5.community channel.

- Improved user experience when connecting to an account with trading restrictions.

Trading can be limited for various reasons: investor mode connection; a trading agreement has not been accepted; broker verification has not been completed and others. Previously, the reason for the unavailability of trading functions was not explained.

Now, if trading is restricted, the order placing button in the Trade section will be grayed out. When pressed, it will show the relevant information and recommendations.

- Improved workflow with SSL certificates which are used for advanced authentication.

Now, when the user connects to an account with advanced authentication, the app will show a brief description of the required actions.

A certificate can be imported from a PFX file. Save the necessary file in the Files app and then use the import function in the start dialog.

It has also become possible to import certificates to files, which enables the use of certificates on other devices. To do this, go to Settings \ Certificates and select "Export" in the certificate menu.

- Construction of price charts has been transferred to Metal, which is the latest-generation graphics API used in Apple devices. This significantly increases the chart, indicator and object rendering performance.

- Fixed substitution of Stop Loss and Take Profit levels in the Depth of Market. For FIFO accounts, stop levels will be automatically set in accordance with the stop levels of existing open positions for the same instrument. This process is required to comply with the FIFO rule.

- Fixed requoting. When a requote is returned, the user is given a short time to accept or to decline the new prices. If no action is taken within the required time frame, the request is automatically rejected and the requote window is automatically closed.

- Fixed display of time in the Chart section when using the dark interface theme.

Terminal

- Terminal: Updated translations of the user interface.

- Fixes based on crash logs.

Web Terminal

- Fixed errors in 2FA/TOTP authentication.

Web Terminal

- Added support for 2FA/TOTP authentication using Google Authenticator and similar apps.

The 2FA/TOTP authentication protects a trading account from unauthorized access even if its login and password are leaked. Authentication using Time-based One-time Password Algorithm (TOTP) can be implemented using various mobile apps. The most popular of them are Google Authenticator, Microsoft Authenticator, LastPass Authenticator and Authy. Now you can connect to your account in the Trade Master 9 client terminal using one-time passwords generated by such Authenticator apps.

To enable the two-factor authentication option, connect to your account via Trade Master 9 Web Terminal. Then click on your account in the menu and select "Enable 2FA/TOTP" in the newly opened dialog. Run the Authenticator app on your mobile device, click "+" to add your trading account and scan the QR code from the terminal. Enter the generated code in the "One-time password" field and click "Enable 2FA". A secret will be registered for your account on the broker's trading server.

The saved secret will be used in the Authenticator app to generate an OTP code every time you connect to your account. Each password is valid for 30 seconds. After that a new one is generated.

A backup code is also displayed in the QR code dialog for linking to the generator. Save it in a secure place. If you lose access to your linked device, the code will allow you to add your account to the Authenticator app again.

If you decide to remove the stored secret from the Authenticator app, you should first disable 2FA/TOTP authentication using the appropriate account menu command. If the new 2FA/TOTP authentication method is not available on your account, please contact your broker.

- Expanded the amount of data

displayed in the Market Watch. Now, in addition to the current Bid/Ask

prices and the price change percentage, you can see:

- Maximum and minimum Bid/Ask price for the current trading session

- Open prices of the current trading session and close prices of the previous trading session

Use the context menu to customize the displayed information:

- Added risk notification display when a corresponding setting is enabled on the broker's side. Some regulators require that traders read and accept the notification before trading.

- Fixed display of the top toolbar on iPhone models featuring a notch at the top of the screen. Previously, it occasionally could cover the panel buttons.

- Fixed

display of the account final financial parameters (profit, equity,

etc.) in the Google Chrome browser. Sometimes, they were not updated.

Terminal

- Optimized and greatly accelerated the demo account opening dialog.

- Updated translations of the user interface.

- Fixes based on crash logs.

MQL5

- Added new methods to the COpenCL class of the Standard Library:

- BufferFromMatrix — filling the device buffer with data from the matrix

- BufferToMatrix — reading data from the device buffer into the matrix

- ContextCreate — creating the device context (the first part of the Initialize method)

- ProgramCreate — creating a program based on the OpenCL source code (the second part of the Initialize method)

- ContextClean — releasing all data belonging to the device context (similar to the Shutdown method but without removing the context)

- GetDeviceInfoInteger — receiving an integer device property

- GetKernelInfoInteger — receiving an integer kernel property

- GetDeviceInfo — receiving any single integer device property not present in the ENUM_OPENCL_PROPERTY_INTEGER enumeration

GetDeviceInfo usage example:

long preferred_workgroup_size_multiple=OpenCL.GetDeviceInfo(0x1067);

- Added the TERMINAL_CPU_NAME and TERMINAL_OS_VERSION values to the ENUM_TERMINAL_INFO_STRING enumeration. They allow receiving the user's CPU and OS names.

void OnStart() { string cpu,os; //--- cpu=TerminalInfoString(TERMINAL_CPU_NAME); os=TerminalInfoString(TERMINAL_OS_VERSION); PrintFormat("CPU: %s, OS: %s",cpu,os); }

Result:

CPU: Intel Xeon E5-2630 v4 @ 2.20GHz, OS: Windows 10 build 19045

- Fixed operation of the "table_or_sql" parameter in the DatabasePrint and DatabaseExport functions. Now it is able to pass a table name in addition to a SQL query.

MetaEditor

- Fixed the check for the maximum number of displayable columns in the database. Up to 64 columns can now be displayed.

- Fixed operation of breakpoints in short constructions like IF[ if(cond) break; ].

Terminal

- Added 2FA/TOTP authentication using Google Authenticator and similar apps.

The 2FA/TOTP authentication protects a trading account from unauthorized access even if its login and password are leaked. Authentication using Time-based One-time Password Algorithm (TOTP) can be implemented using various mobile apps. The most popular of them are Google Authenticator, Microsoft Authenticator, LastPass Authenticator and Authy. Now you can connect to your account in the Trade Master 9 client terminal using one-time passwords generated by such Authenticator apps.

To enable the two-factor authentication option, connect to your account and execute the "Enable 2FA/TOTP" command in the account context menu. Run the Authenticator app on your mobile device, click "+" to add your trading account and scan the QR code from the terminal. Enter the generated code in the "One-time password" field and click "Enable 2FA". A secret will be registered for your account on the broker's trading server.

The saved secret will be used in the Authenticator app to generate an OTP code every time you connect to your account. Each password is valid for 30 seconds. After that a new one is generated.

If you decide to remove the stored secret from the Authenticator app, you should first disable 2FA/TOTP authentication using the appropriate account context menu command. If the new 2FA/TOTP authentication method is not available on your account, please contact your broker.

MQL5

- Fixed operation of the CopyTicks function for custom trading instruments. When working with custom symbols, previous session's initial ticks could be returned instead of requested data, under certain conditions.

- Added new enumeration values to get the last OpenCL error code and text description.

- Value CL_LAST_ERROR (code 4094) has been added to the ENUM_OPENCL_PROPERTY_INTEGER enumeration

When obtaining the last OpenCL error via CLGetInfoInteger, the handle parameter is ignored. Error descriptions: https://registry.khronos.org/OpenCL/specs/3.0-unified/html/OpenCL_API.html#CL_SUCCESS.

For an unknown error code, the string "unknown OpenCL error N" is returned, where N is the error code.

Example://--- the first handle parameter is ignored when obtaining the last error code int code = (int)CLGetInfoInteger(0,CL_LAST_ERROR);

- Value CL_ERROR_DESCRIPTION (4093) has been added to the ENUM_OPENCL_PROPERTY_STRING enumeration.

A text error description can be obtained using CLGetInfoString. Error descriptions: https://registry.khronos.org/OpenCL/specs/3.0-unified/html/OpenCL_API.html#CL_SUCCESS.

When using CL_ERROR_DESCRIPTION, an error code should be passed as the handle parameter in CLGetInfoString. If CL_LAST_ERROR is passed instead of the error code, the function will return the last error description.

Example://--- get the code of the last OpenCL error int code = (int)CLGetInfoInteger(0,CL_LAST_ERROR); string desc; // to get the text description of the error //--- use the error code to get the text description of the error if(!CLGetInfoString(code,CL_ERROR_DESCRIPTION,desc)) desc = "cannot get OpenCL error description, " + (string)GetLastError(); Print(desc); //--- to get the description of the last OpenCL error without receiving the code, pass CL_LAST_ERROR if(!CLGetInfoString(CL_LAST_ERROR,CL_ERROR_DESCRIPTION, desc)) desc = "cannot get OpenCL error description, " + (string)GetLastError(); Print(desc);

The internal enumeration name is passed as the error description. Its explanation can be found at https://registry.khronos.org/OpenCL/specs/3.0-unified/html/OpenCL_API.html#CL_SUCCESS. For example, the CL_INVALID_KERNEL_ARGS value means "Returned when enqueuing a kernel when some kernel arguments have not been set or are invalid."

- Fixed operation of the matrix::MatMul method. When working with large matrices, the terminal could crash on certain sizes.

Trade Master 9 WebTerminal

-

In the mobile

version we have implemented trading history sorting and filtering by

depth. Use the top-panel commands to customize the history display:

Operations can be sorted by the main parameters, such as date, ticket, symbol and volume, among others.

-

Improved access to trading account details.

- In the desktop version the current account data is clickable. Click on the account to view its details.

- In the mobile version the current account is displayed under the Settings section. Click on the account to view its details.

- Fixed display of the account type in the account management window.

- Fixed equity and free margin display after refreshing the web terminal page in mobile browsers.

- Fixed bottom bar display in Firefox mobile browser

Terminal

- Fixed equity and balance graph calculations in the trading report.

MQL5

-

New behavior of typename(expr). The updated function returns the full type with modifiers and dimensions (for arrays):

class A { }; void OnStart(void) { const A *const arr[][2][3]={}; Print(typename(arr)); }

Result:

"class A const * const [][2][3]"

Terminal

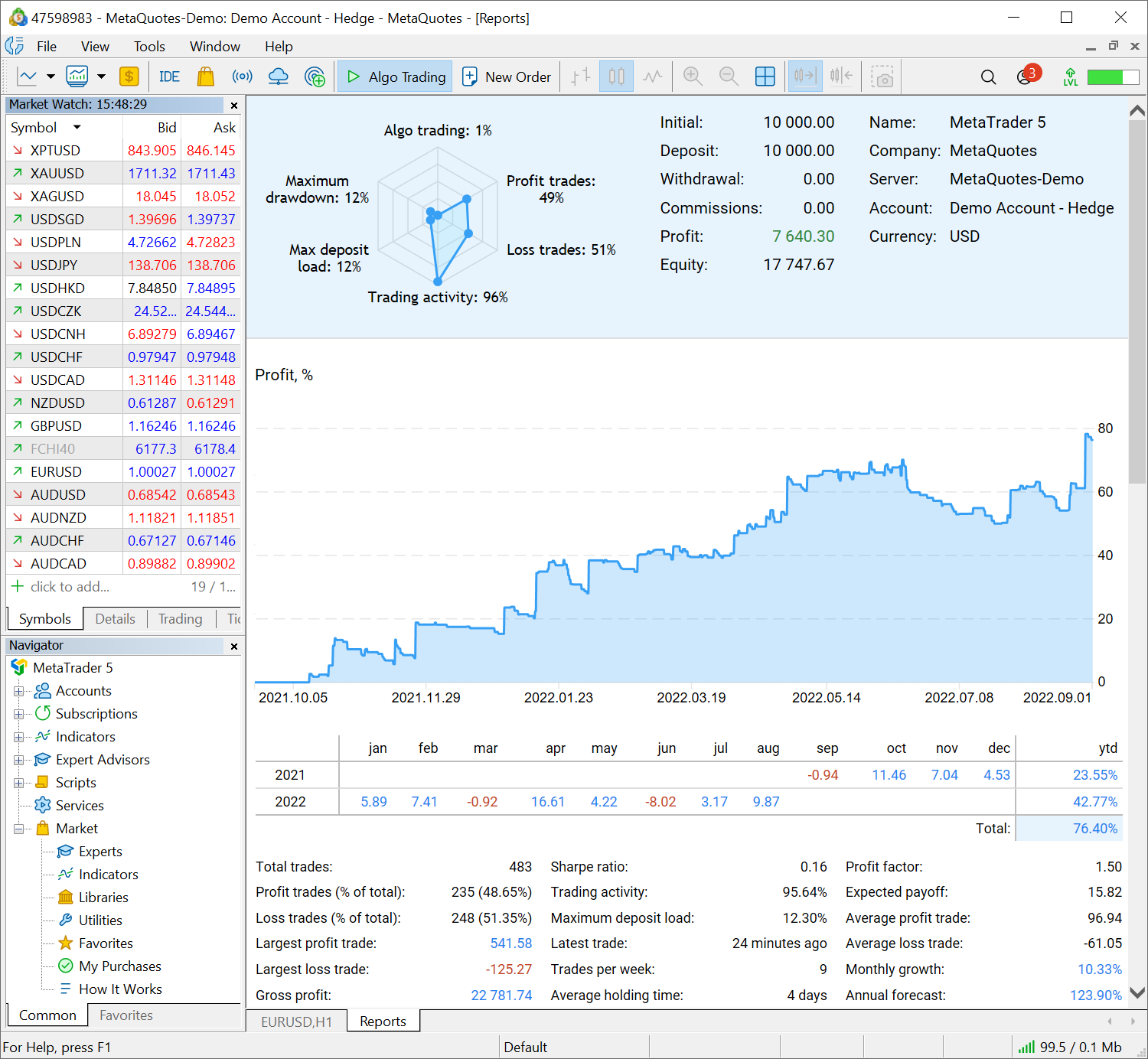

- A new command has been added to the context menu of the Trade and History sections, to enable access to the new trading report.

The trading report provides the following performance data:

- Graphs and tables visualizing monthly growth metrics

- Equity chart

- Radar chart which enables quick account state evaluation

- Trading statistics by instrument

- A variety of additional metrics for trading analysis

- Fixed initial deposit calculations in the trading report.

- Fixed setting of Stop Loss and Take Profit levels when using using the quick trading panel in the chart and Market Watch. The levels could be inherited from previously opened positions even when the inheritance was not required (the relevant functionality is implemented for FIFO-based accounts).

- Updated user interface translations.

MQL5

- Fixed a compiler bug which enabled access to a structure field using a constant string with the field name value.

- MQL5: Fixed checking of key states using the TerminalInfoInteger(TERMINAL_KEYSTATE_*) function.

Fixed errors reported in crash logs.

Trade Master 9 WebTerminal build 3500

- Fixed position closing upon requotes.

- Fixed reconnection to the server after maximizing a browser window which has been inactive for a long time.

- Fixed display of credit funds.

- ther improvements and fixes.

The new Web Terminal provides full-featured support for mobile devices. The interface will automatically adapt to the screen size, enabling efficient operations from iOS and Android phones and tablets:

Also, the Web Terminal features a lot of fixes and improvements.

The new Trade Master 9 Web Terminal supports the full set of trading functions. It enables users to:

- Work with demo and live accounts

- Receive any financial symbol quotes

- Trade in any markets

- Analyze symbol quotes using more than 30 indicators and 20 graphical objects

- Use Economic Calendar data for fundamental analysis

Terminal

- Extended task manager features. The new version enables more accurate monitoring of consumed resources.

- Added stack size display for threads.

- Added display of the number of context switches.

- Added recognition of system and third-party DLL threads.

- Added display of kernel mode operating time. An increase in this metric compared to the time spent in user mode can indicate system-level issues: drivers problems, hardware errors or slow hardware. For further details, please read the Microsoft Documentation.

- Added display of user mode operating time.

- New OpenCL tab in terminal settings for managing available devices. The new OpenCL manager enables explicit specification of devices to be used for calculations.

- Added indication of Stop Loss and Take Profit levels in the Depth of Market for accounts operating in FIFO mode (the mode can be enabled on the broker's side).

According to the FIFO rule, positions for each instrument can only be closed in the same order in which they were opened. To ensure FIFO-compliant position closing by stop levels, the following logic has been implemented on the client terminal side:

If multiple positions exist for the same instrument, the placing of stop levels for any of the positions causes the same levels to be placed for all other positions as well. Accordingly, if a level triggers, all positions will be closed in a FIFO-compliant order.

Now, when the user opens the Depth of Market for an instrument which already has open positions for, the levels of existing positions (if any) are automatically specified in the Stop Loss and Take Profit fields.

- Fixed deletion of Stop Loss and Take Profit levels using X buttons in the Toolbox\Trade window. The error occurred when the quick trading function was disabled. A click on the button will open a trading dialog with an empty value of the relevant level.

- Fixed graph captions and final commission calculations in the trading report. The section could show incorrect Profit in report statistics and incorrect values in Equity and Balance graph tooltips.

MQL5

- Added vector and matrix methods CopyTicks and CopyTicksRange. They enable easy copying of tick data arrays into vectors and matrices.

bool matrix::CopyTicks(string symbol,uint flags,ulong from_msc,uint count); bool vector::CopyTicks(string symbol,uint flags,ulong from_msc,uint count); bool matrix::CopyTicksRange(string symbol,uint flags,ulong from_msc,ulong to_msc); bool matrix::CopyTicksRange(string symbol,uint flags,ulong from_msc,ulong to_msc);

The copied data type is specified in the 'flags' parameter using the ENUM_COPY_TICKS enumeration. The following values are available:

COPY_TICKS_INFO = 1, // ticks resulting from Bid and/or Ask changes COPY_TICKS_TRADE = 2, // ticks resulting from Last and Volume changes COPY_TICKS_ALL = 3, // all ticks having changes COPY_TICKS_TIME_MS = 1<<8, // time in milliseconds COPY_TICKS_BID = 1<<9, // Bid price COPY_TICKS_ASK = 1<<10, // Ask price COPY_TICKS_LAST = 1<<11, // Last price COPY_TICKS_VOLUME = 1<<12, // volume COPY_TICKS_FLAGS = 1<<13, // tick flags

If multiple data types are selected (only available for matrices), the order of the rows in the matrix will correspond to the order of values in the enumeration.

- Expanded features of matrix::Assign and vector::Assign methods.

Now the matrix can be assigned a one-dimensional array or vector:

bool matrix::Assign(const vector &vec);

The result will be a one-row matrix.

Also, a matrix can now be assigned to a vector (matrix smoothing will be performed):

bool vector::Assign(const matrix &mat);

- Added Swap methods for vectors and matrices.

bool vector::Swap(vector &vec); bool vector::Swap(matrix &vec); bool vector::Swap(double &arr[]); bool matrix::Swap(vector &vec); bool matrix::Swap(matrix &vec); bool matrix::Swap(double &arr[]);

Each array, vector or matrix refers to a memory buffer which contains the elements of that object. The Swap method actually swaps pointers to these buffers without writing the elements to memory. Therefore, a matrix remains a matrix, and a vector remains a vector. Swapping a matrix and a vector will result in a one-row matrix with vector elements and a vector with matrix elements in a flat representation (see the Flat method).

//+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { //--- matrix a= {{1, 2, 3}, {4, 5, 6}}; Print("a before Swap: \n", a); matrix b= {{5, 10, 15, 20}, {25, 30, 35, 40}, {45, 50, 55, 60}}; Print("b before Swap: \n", b); //--- swap matrix pointers a.Swap(b); Print("a after Swap: \n", a); Print("b after Swap: \n", b); /* a before Swap: [[1,2,3] [4,5,6]] b before Swap: [[5,10,15,20] [25,30,35,40] [45,50,55,60]] a after Swap: [[5,10,15,20] [25,30,35,40] [45,50,55,60]] b after Swap: [[1,2,3] [4,5,6]] */ vector v=vector::Full(10, 7); Print("v before Swap: \n", v); Print("b before Swap: \n", b); v.Swap(b); Print("v after Swap: \n", v); Print("b after Swap: \n", b); /* v before Swap: [7,7,7,7,7,7,7,7,7,7] b before Swap: [[1,2,3] [4,5,6]] v after Swap: [1,2,3,4,5,6] b after Swap: [[7,7,7,7,7,7,7,7,7,7]] */ }

The Swap() method also enables operations with dynamic arrays (fixed-sized arrays cannot be passed as parameters). The array can be of any dimension but of an agreed size, which means that the total size of a matrix or vector must be a multiple of the array's zero dimension. The array's zero dimension is the number of elements contained at the first index. For example, for a dynamic three-dimensional array 'double array[][2][3]', the zero dimension is the product of the second and third dimension sizes: 2x3=6. So, such an array can only be used in the Swap method with matrices and vectors whose total size is a multiple of 6: 6, 12, 18, 24, etc.

Consider the following example:

//+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { //--- fill the 1x10 matrix with the value 7.0 matrix m= matrix::Full(1, 10, 7.0); Print("matrix before Swap:\n", m); //--- try to swap the matrix and the array double array_small[2][5]= {{1, 2, 3, 4, 5}, {6, 7, 8, 9, 10}}; Print("array_small before Swap:"); ArrayPrint(array_small); if(m.Swap(array_small)) { Print("array_small after Swap:"); ArrayPrint(array_small); Print("matrix after Swap: \n", m); } else // the matrix size is not a multiple of the first array dimension { Print("m.Swap(array_small) failed. Error ", GetLastError()); } /* matrix before Swap: [[7,7,7,7,7,7,7,7,7,7]] array_small before Swap: [,0] [,1] [,2] [,3] [,4] [0,] 1.00000 2.00000 3.00000 4.00000 5.00000 [1,] 6.00000 7.00000 8.00000 9.00000 10.00000 m.Swap(array_small) failed. Error 4006 */ //--- use a larger matrix and retry the swap operation double array_static[3][10]= {{1, 2, 3, 4, 5, 6, 7, 8, 9, 10}, {2, 4, 6, 8, 10, 12, 14, 16, 18, 20}, {3, 6, 9, 12, 15, 18, 21, 24, 27, 30} }; Print("array_static before Swap:"); ArrayPrint(array_static); if(m.Swap(array_static)) { Print("array_static after Swap:"); ArrayPrint(array_static); Print("matrix after Swap: \n", m); } else // a static array cannot be used to swap with a matrix { Print("m.Swap(array_static) failed. Error ", GetLastError()); } /* array_static before Swap: [,0] [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [0,] 1.00000 2.00000 3.00000 4.00000 5.00000 6.00000 7.00000 8.00000 9.00000 10.00000 [1,] 2.00000 4.00000 6.00000 8.00000 10.00000 12.00000 14.00000 16.00000 18.00000 20.00000 [2,] 3.00000 6.00000 9.00000 12.00000 15.00000 18.00000 21.00000 24.00000 27.00000 30.00000 m.Swap(array_static) failed. Error 4006 */ //--- another attempt to swap an array and a matrix double array_dynamic[][10]; // dynamic array ArrayResize(array_dynamic, 3); // set the first dimension size ArrayCopy(array_dynamic, array_static); //--- now use a dynamic array for swap if(m.Swap(array_dynamic)) { Print("array_dynamic after Swap:"); ArrayPrint(array_dynamic); Print("matrix after Swap: \n", m); } else // no error { Print("m.Swap(array_dynamic) failed. Error ", GetLastError()); } /* array_dynamic after Swap: [,0] [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [0,] 7.00000 7.00000 7.00000 7.00000 7.00000 7.00000 7.00000 7.00000 7.00000 7.00000 matrix after Swap: [[1,2,3,4,5,6,7,8,9,10,2,4,6,8,10,12,14,16,18,20,3,6,9,12,15,18,21,24,27,30]] */ }

- Added LossGradient method for vectors and matrices. This method calculates a vector or matrix of partial derivatives of the loss function on predicted values. In linear algebra, such a vector is referred to as a gradient and is used in machine learning.

vector vector::LossGradient(const vector &expected,ENUM_LOSS_FUNCTION loss) const; matrix matrix::LossGradient(const matrix &expected,ENUM_LOSS_FUNCTION loss) const;

- Enabled use of FOREIGN KEYS in SQLite to enforce relationships between tables in SQL queries. Example:

CREATE TABLE artist( artistid INTEGER PRIMARY KEY, artistname TEXT ); CREATE TABLE track( trackid INTEGER, trackname TEXT, trackartist INTEGER, FOREIGN KEY(trackartist) REFERENCES artist(artistid) );

- Fixed selection of the appropriate class method depending on the method and object constness.

MetaEditor

- Increased allowable length of comments in commits to MQL5 Storage. Detailed comments when committing changes to the repository are considered good practice when working in large projects, but previously the comment length has been limited to 128 characters. The allowed length is now up to 260 characters.

MetaTester

- Increased sensitivity of the testing speed switch in visual mode.

Fixed errors reported in crash logs.

Terminal

- Added new account trading performance report. It is similar to the already familiar Signals

reports in terms of statistics availability and data presentation. The

following performance data will be available in the platform:

- Graphs and tables visualizing monthly growth metrics

- Equity chart

- Radar chart which enables quick account state evaluation

- Trading statistics by instrument

- A variety of additional metrics for trading analysis

The report can be viewed directly in the platform, without the need to export it to a file. To open it, select Reports in the View menu.

- Graphs and tables visualizing monthly growth metrics

- Fixed options board filling for Call and Put contracts with unmatching quantity or symbol type.

- Fixed position selection in the Trade dialog during Close by operations. The error occurred for opposite order lists sorted by any column other than the ticket.

- Accelerated platform logging.

- Fixed display of comments on custom symbol charts.

MQL5

- Fixed CArrayList::LastIndexOf function operation. Previously, it always returned -1 instead of the index of the last found element.

- Added new matrix and vector method - Assign. It replaces matrix/vector

elements with the passed matrix/vector or array data.

bool vector<TDst>::Assign(const vector<TSrc> &assign); bool matrix<TDst>::Assign(const matrix<TSrc> &assign);

Example:

//--- copying matrices matrix b={}; matrix a=b; a.Assign(b); //--- copying an array to a matrix double arr[5][5]={{1,2},{3,4},{5,6}}; Print("array arr"); ArrayPrint(arr); b.Assign(arr); Print("matrix b \n",b); /* array arr [,0] [,1] [,2] [,3] [,4] [0,] 1.00000 2.00000 0.00000 0.00000 0.00000 [1,] 3.00000 4.00000 0.00000 0.00000 0.00000 [2,] 5.00000 6.00000 0.00000 0.00000 0.00000 [3,] 0.00000 0.00000 0.00000 0.00000 0.00000 [4,] 0.00000 0.00000 0.00000 0.00000 0.00000 matrix b [[1,2,0,0,0] [3,4,0,0,0] [5,6,0,0,0] [0,0,0,0,0] [0,0,0,0,0]] */

- Added new matrix and vector method - CopyRates. It copies price data arrays into vectors and matrices.

bool matrix::CopyRates(string symbol,ENUM_TIMEFRAMES period,ulong rates_mask,ulong from,ulong count); bool vector::CopyRates(string symbol,ENUM_TIMEFRAMES period,ulong rates_mask,ulong from,ulong count);

The copied data type is specified in the rates_mask parameter using the ENUM_COPY_RATES enumeration. The following values are available:

COPY_RATES_OPENThe last two values enable the simultaneous selection of multiple bar parameters: Open, High, Low, Close and time.

COPY_RATES_HIGH

COPY_RATES_LOW

COPY_RATES_CLOSE

COPY_RATES_TIME

COPY_RATES_VOLUME_TICK

COPY_RATES_VOLUME_REAL

COPY_RATES_SPREAD

COPY_RATES_OHLC

COPY_RATES_OHLCT

If multiple data types are selected (only available for matrices), the order of the rows in the matrix will correspond to the order of values in the enumeration.

- Fixed display of Text Label objects. When using OBJPROP_XOFFSET and OBJPROP_YOFFSET properties, a wrong image fragment could be displayed on the chart.

-

Fixed error when changing a constant parameter which has been passed to a function as an object pointer reference.

The const specifier declares a variable as a constant to prevent it from being changed during program execution. It only allows one-time variable initialization during declaration. An example of constant variables in the OnCalculate function:

int OnCalculate (const int rates_total, // price[] array size const int prev_calculated, // bars processed on previous call const int begin, // meaningful data starts at const double& price[] // array for calculation );

The below example contains a compiler error which allowed an implicit pointer casting for reference parameters:

class A {}; const A *a = new A; void foo( const A*& b ) { b = a; } void OnStart() { A *b; foo(b); // not allowed Print( a,":",b ); }

The compiler will detect such illegal operations and will return the relevant error.

MetaEditor

- Fixed display of complex number references in the debugger.

- Improved MQL5 Cloud Protector. Previously, file protection could fail under certain conditions.

- Fixed errors reported in crash logs.

New Trade Master 9 Web Terminal

We

have released a revised Trade Master 9 Web Terminal which features an

updated interface and a redesigned core. The new interface is similar to

the terminal version for iPad:

It also features a plethora of new functions:

- Ability to request real accounts with the detailed registration form and document submission options

- Support for price data subscriptions and the ability to receive delayed quotes

- More analytical objects with convenient management options

- Market entries and exits displayed on charts

- Economic Calendar events displayed on charts

- Convenient configuration of instruments in the Market Watch, along with the daily price change data

- Simplified interface to assist beginners in getting started with the terminal: removed chart context menu and top menu; all chart control commands, objects and indicators are available on the left-hand side and top panels, while other commands can be accessed through the hamburger menu

- Interface dark mode

Try the new web terminal at www.mql5.com right now. It will soon become available for your brokers.

Terminal

- Added automatic opening of a tutorial

during the first connection to a trading account. This will assist

beginners in learning trading basics and in exploring platform features.

The tutorial is divided into several sections, each of which provides

brief information on a specific topic. The topic completion progress is

shown with a blue line.

- Fixed 'Close profitable'/'Close losing' bulk operations.

Previously, the platform used opposite positions if they existed. For

example, if you had two losing Buy positions for EURUSD and one

profitable Sell position for EURUSD, all three positions would be closed

during the 'Close losing' bulk operation. Buy and Sell would be closed

by a 'Close by' operation, while the remaining Buy would be closed by a

normal operation. Now the commands operate properly: they only close the

selected positions, either profitable or losing.

- Fixed display of negative historical prices. Such prices will appear correctly for all timeframes.

- Optimized and significantly reduced system resource consumption by the terminal.

- Updated fundamental database for trading instruments. The number of

data aggregators available for exchange instruments has been expanded to

15. Users will be able to access information on even more tickers via

the most popular economic aggregators.

About 7,000 securities and more than 2,000 ETFs are listed on the global exchange market. Furthermore, exchanges provide futures and other derivatives. The Trade Master 9 platform offers access to a huge database of exchange instruments. To access the relevant fundamental data, users can switch to the selected aggregator's website in one click directly from the Market Watch. For convenience, the platform includes a selection of information sources for each financial instrument.

- Fixed Stop Loss and Take Profit indication in the new order placing

window. For FIFO accounts, stop levels will be automatically set in

accordance with the stop levels of existing open positions for the same

instrument. This procedure is required to comply with the FIFO rule.

MQL5

- Mathematical functions can now be applied to matrices and vectors.

We continue expanding algorithmic trading and machine learning capabilities in the Trade Master 9 platform. Previously, we have added new data types: matrices and vectors, which eliminate the need to use arrays for data processing. More than 70 methods have been added to MQL5 for operations with these data types. The new methods enable linear algebra and statistics calculations in a single operation. Multiplication, transformation and systems of equations can be implemented easily, without extra coding. The latest update includes mathematical functions.

Mathematical functions were originally designed to perform relevant operations on scalar values. From this build and onward, most of the functions can be applied to matrices and vectors. These include MathAbs, MathArccos, MathArcsin, MathArctan, MathCeil, MathCos, MathExp, MathFloor, MathLog, MathLog10, MathMod, MathPow, MathRound, MathSin, MathSqrt, MathTan, MathExpm1, MathLog1p, MathArccosh, MathArcsinh, MathArctanh, MathCosh, MathSinh, and MathTanh. Such operations imply element-wise handling of matrices and vectors. Example:

//--- matrix a= {{1, 4}, {9, 16}}; Print("matrix a=\n",a); a=MathSqrt(a); Print("MatrSqrt(a)=\n",a); /* matrix a= [[1,4] [9,16]] MatrSqrt(a)= [[1,2] [3,4]] */

For MathMod and MathPow, the second element can be either a scalar or a matrix/vector of the appropriate size.

The following example shows how to calculate the standard deviation by applying math functions to a vector.